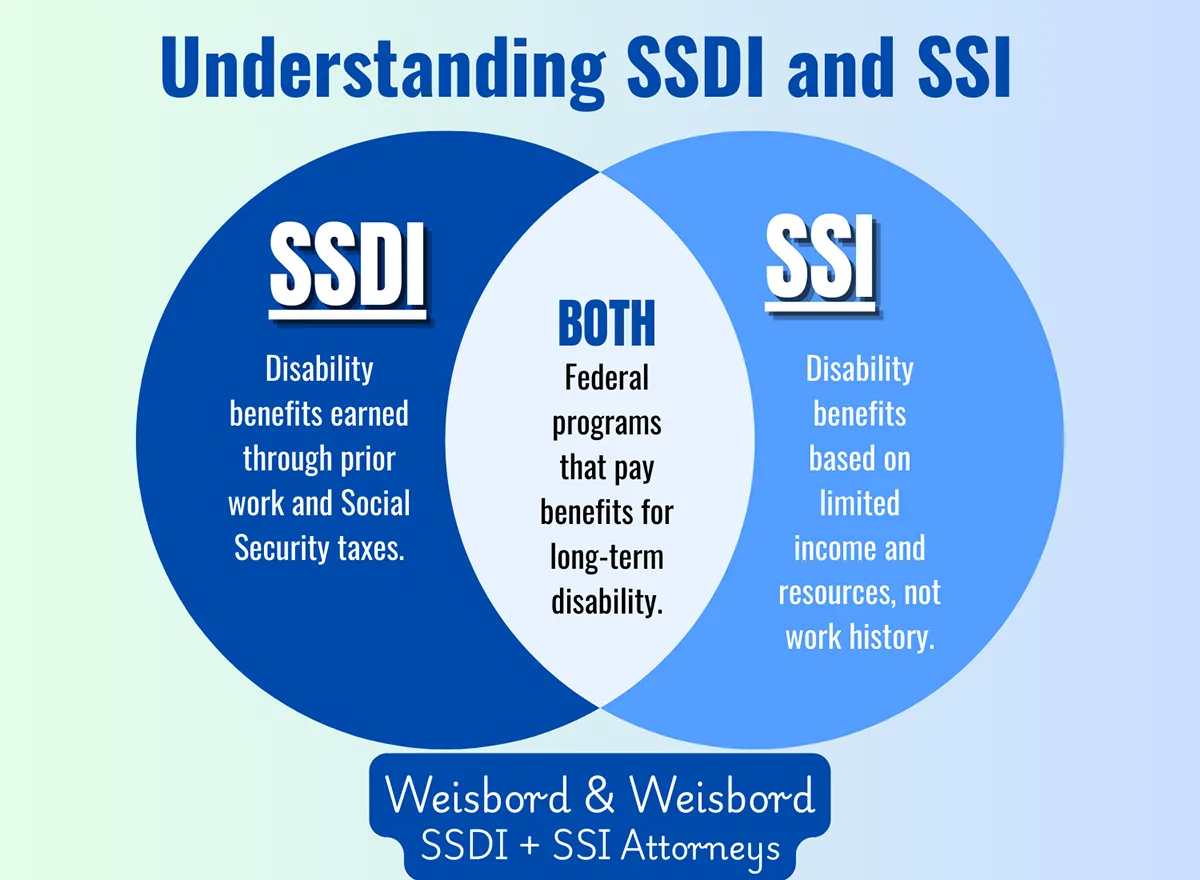

SSDI and SSI Are Not Two Versions of the Same Program

People typically apply for Social Security disability benefits because work has become unsustainable. The medical issue may have been building for years, or it may have come abruptly, but the result is the same. Income drops while expenses continue. At some point, someone mentions “disability,” and the assumption follows naturally that there is a single federal program meant to address that gap. What most people discover instead is a pair of acronyms, SSDI and SSI, that look interchangeable on the surface but operate according to fundamentally different rules.

That confusion is understandable, but it is not harmless. The Social Security Administration administers both programs. Both involve disability determinations. Both can result in monthly payments. Yet they exist for different reasons, are funded differently, and apply to different populations. Understanding the distinction is not a technical exercise. It determines eligibility, payment timing, benefit amount, and which types of financial decisions remain safe while a claim is pending.

SEE COMPARISON CHART = Button goes to PDF

The Difference Is Structural, Not Medical

That distinction begins with how the law itself frames disability. One of the most persistent misconceptions is that SSDI and SSI represent different levels or types of disability. That is not how the system works. The medical standard used to evaluate disability is largely the same across both programs. Social Security applies a strict definition that centers on whether a medically determinable impairment prevents substantial gainful activity and is expected to last at least twelve months or result in death. Approval turns on evidence, function, and duration, not on which acronym appears on the application.

Where the programs truly diverge is not in how disability is defined, but in what must be true in addition to disability before payment is possible. SSDI and SSI are built on different eligibility foundations. One is tied to prior work. The other is tied to present financial need. That single structural difference explains most of the practical consequences people experience once they enter the system.

SSDI Is Disability Coverage Earned Through Work

Understanding SSDI begins with its role within the Social Security system. Social Security Disability Insurance is funded by workers’ contributions during their careers. Every paycheck that includes FICA contributions builds insured status, and SSDI functions as the disability arm of that insurance framework. The program is designed to replace a portion of lost earnings for a worker who has paid into the system and can no longer sustain employment due to a qualifying medical condition.

Eligibility for SSDI, therefore, depends heavily on work history. Social Security looks at whether the individual worked in covered employment long enough and recently enough to be considered insured at the time disability began. The question is not whether someone ever worked, but whether sufficient work credits exist within a defined period before the onset of disability. Someone with a long career who becomes disabled later in life is often insured. Someone with a limited or sporadic work history may not be eligible, even if their medical condition is severe.

That structure also explains why SSDI does not impose limits on savings, assets, or household resources. It is not a needs-based program. It is an insurance benefit tied to earnings, and benefit amounts reflect that history. Two people with identical medical conditions may receive very different SSDI payments because the calculation is based on lifetime covered earnings, not current financial hardship.

SSI Exists to Provide a Financial Floor

SSI operates on a different premise entirely. Supplemental Security Income exists to ensure that people who are elderly, blind, or disabled are not left without basic income simply because they never accumulated sufficient work history. Unlike SSDI, SSI is not funded through payroll taxes. It is paid from general federal revenues and functions as a needs-based safety net rather than an earned benefit.

Because of that design, SSI eligibility hinges on income and resources. Social Security evaluates not only disability but also income, assets, and whether those figures fall below strict statutory thresholds. The program assumes that if resources exist above those limits, SSI is not appropriate, regardless of medical severity.

This is often the point where expectations collide with reality. SSI does not simply look at disability. It looks at bank accounts, household support, and ongoing income streams. A modest SSDI payment, a pension, or even consistent family support can reduce or eliminate SSI eligibility. Conversely, someone who has never worked or whose work history does not meet insured-status requirements may qualify for SSI precisely because no other support is available.

Why the Same Person Can Sometimes Receive Both

Once the structural purposes of the two programs are clear, it becomes easier to understand how overlap can occur. The fact that SSDI and SSI serve different purposes does not mean they are mutually exclusive. In some cases, a person qualifies for both simultaneously. This typically happens when SSDI eligibility exists, but the SSDI benefit amount is low enough that total income still falls below SSI’s financial threshold.

In those situations, SSI functions as a supplement rather than a replacement, bringing income up to the minimum level the law allows. This overlap adds to confusion because payments may be combined, arrive from the same agency, and be discussed under the umbrella of “disability.” Without a clear understanding of the structural distinction, it can be difficult to see why one portion of a payment responds to earnings history while the other responds to income changes.

Payment Timing and Health Coverage Follow the Program

The program under which benefits are paid also determines how support unfolds over time. SSDI includes a mandatory waiting period tied to the established onset date of disability, and Medicare eligibility typically follows after a qualifying period. SSI does not include the same waiting structure, and Medicaid eligibility is often immediate, depending on state rules.

These differences are not administrative quirks or processing artifacts. They reflect the underlying purpose of each program. SSDI assumes prior attachment to the workforce and delays payment to confirm long-term disability. SSI assumes immediate financial vulnerability and prioritizes basic support and access to care.

Clarity Comes from Structure, Not Acronyms

Work with the Best Social Security Attorney Philadelphia has to Offer.

SSDI and SSI are not variations of the same benefit. They are parallel programs designed to address different gaps. One replaces earnings that can no longer be earned. The other prevents destitution when there is no earnings record. Once that distinction is understood, the rest of the system becomes easier to navigate.

Disability law is often described as complex, but that complexity usually arises from treating overlapping systems as interchangeable. When SSDI and SSI are understood on their own terms, the path forward stops feeling arbitrary and starts feeling definable. At Weisbord & Weisbord, this clarity is not theoretical. It is the foundation of how we help people navigate SSDI and SSI with intention rather than guesswork.

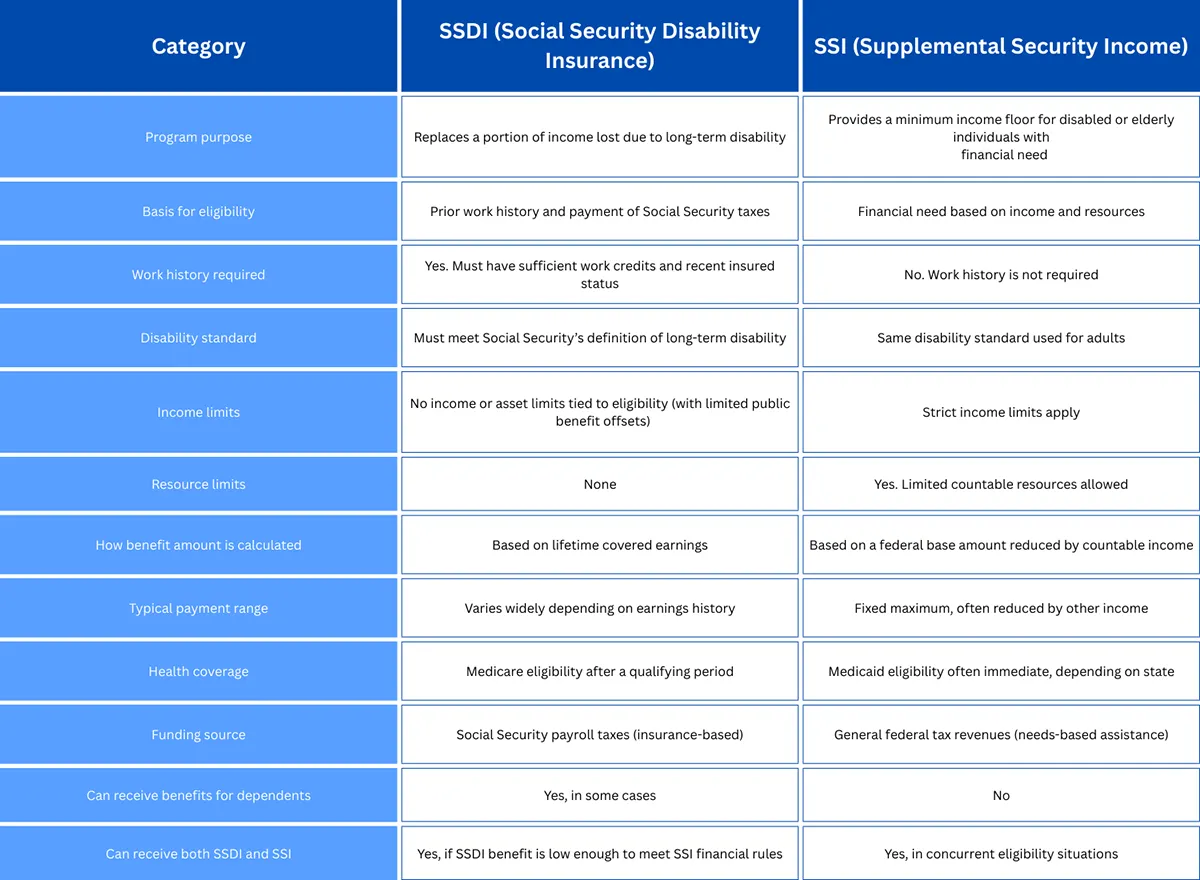

SSDI vs. SSI: Key Differences at a Glance

| Category | SSDI (Social Security Disability Insurance) | SSI (Supplemental Security Income) |

| Program purpose | Replaces a portion of income lost due to long-term disability | Provides a minimum income floor for disabled or elderly individuals with financial need |

| Basis for eligibility | Prior work history and payment of Social Security taxes | Financial need based on income and resources |

| Work history required | Yes. Must have sufficient work credits and recent insured status | No. Work history is not required |

| Disability standard | Must meet Social Security’s definition of long-term disability | Same disability standard used for adults |

| Income limits | No income or asset limits tied to eligibility (with limited public benefit offsets) | Strict income limits apply |

| Resource limits | None | Yes. Limited countable resources allowed |

| How benefit amount is calculated | Based on lifetime covered earnings | Based on a federal base amount reduced by countable income |

| Typical payment range | Varies widely depending on earnings history | Fixed maximum, often reduced by other income |

| Health coverage | Medicare eligibility after a qualifying period | Medicaid eligibility often immediate, depending on state |

| Funding source | Social Security payroll taxes (insurance-based) | General federal tax revenues (needs-based assistance) |

| Can receive benefits for dependents | Yes, in some cases | No |

| Can receive both SSDI and SSI | Yes, if SSDI benefit is low enough to meet SSI financial rules | Yes, in concurrent eligibility situations |

Related posts:

SSDI vs. SSI in Philadelphia: Eligibility, Benefits, and Key Differences

SSDI vs. SSI in Philadelphia: Eligibility, Benefits, and Key Differences

Am I Eligible to Apply for Social Security Disability? A Social Security Disability Attorney in Philadelphia Explains

Am I Eligible to Apply for Social Security Disability? A Social Security Disability Attorney in Philadelphia Explains

Working While Applying for or Receiving Social Security Disability in Philadelphia

Working While Applying for or Receiving Social Security Disability in Philadelphia

What Is the 5-Month Waiting Period for SSDI?

What Is the 5-Month Waiting Period for SSDI?